Estimate your project costs instantly with Build It's interactive self-build cost calculator

Calculate NowGet an accurate, detailed cost breakdown of your project

Submit plans

So, you’ve found a plot and can already picture yourself sipping coffee in your designer kitchen – but when you pop into your high street bank to ask about funding, you’re met with blank stares and polite rejections.

High street banks aren’t exactly falling over themselves to offer self build mortgages, but this doesn’t have to mean the end of your bespoke home dream. Here I’m explaining why big banks aren’t quite so friendly, where to look instead, and how you can make yourself look like a five-star borrower to secure funding for your scheme.

A self build mortgage is a loan specifically designed to fund the construction of your own home. Unlike traditional products, which provide a lump sum of money to buy a property, this specialist finance releases funds in stages throughout the duration of the building project. For example, you might get a chunk of the mortgage for purchasing the land, another for achieving the weathertight house shell and so on.

The staged release provides the cash flow you need to cover construction costs. It also reassures the lender, as they only need to release smaller amounts of money to pay for work done, rather than risk handing over a large chunk of cash with nothing to show for it.

Most of them simply see self build as a bit risky. When they lend on an existing property, there’s a physical asset that they could sell if things go wrong. But with a self build, the asset (your new home) doesn’t exist yet. Until the project is completed, they’ve only got a part-finished house, which – according to their conventional lending models – isn’t enough security.

After finding the perfect plot in the Suffolk countryside, Steve and Suzanne Richardson enlisted Cocoon Architects to bring their design ideas to life, and Frame Technologies to erect their efficient timber frame shell. The total costs for the building project were £350,000, (£2,059 per m²) with the land costing £295,000. The project went on to win Best Self Build Home at the 2023 Build It Awards. Photo: Matthew Smith

Perhaps more importantly, high street banks don’t have the knowledge, resource or experience to oversee these kinds of staged releases. Self builds are complicated and require a lender who understands the regulatory requirements, as well as construction timelines and how projects are professionally built. For big banks, this can be more hassle than it’s worth, so they prefer to leave it to specialists who have plenty of experience with construction projects.

This is where building societies step in. Building societies are more flexible and willing to work with self builders because they’re more agile and used to funding development projects. They have processes in place to manage any challenges and can ensure that staged payments work for both them and you.

Some of these building societies, however, do prefer that borrowers work with them through experienced brokers. Why? Because brokers familiar with home building know how to deal with self builders and can manage the risks involved. For the lender, this means fewer surprises and less chance of things going wrong.

So, now you know who will lend to you, how can you be confident of securing the right mortgage? As with any construction project, self building has risks, so lenders will carefully scrutinise applications before they make an offer.

If your application isn’t A1, you might not get the funds you need for the project. To maximise your chances of getting the highest possible self build mortgage offer, it’s vital that you present yourself and your project in the best light. Here’s what to do:

Lenders want to see that you’re responsible with credit, and a strong score helps prove that. Before applying, check your credit report and make sure everything’s in order. Pay down any lingering credit card balances or personal loans, as high debt can make you look financially stretched.

Jonathan and Joanna Lunn left city life behind to build their own contemporary home on a stunning woodland site in the South Downs National Park. The couple worked with Baufritz on a turnkey basis to complete the self build project. The plot of land cost £515,000 and the build cost £1,108,000 (£4,655 per m²)

Big monthly expenses can reduce your mortgage offer, on the basis of affordability. So, it’s worth cutting down wherever possible to demonstrate you can confidently manage the regular repayments.

Cancel underused subscriptions (do you really need five streaming services?) or consider giving these up, at least temporarily. Reduce discretionary spending by cutting back on luxuries that could be seen as non-essential. Dining out every week or splurging on designer clothes might look frivolous to a lender.

Lenders will be concerned about anyone that appears not to have financial control, so if you like a flutter, now’s the time to drop the habit. Remember, making small changes in advance of an application can boost your affordability later, so clean up your finances.

Lenders like to see what they’re backing, so make sure your plans and specifications are professional. They’ll want to understand the finer detail to be certain that your proposals fit with their lender rules.

This isn’t just about the building structure or what claddings you’ll use; they’ll want to assess the value of the finished property, too. It’s best to treat this like a pitch – the more you can do to show that your finished home will be professionally built, high quality and valuable, the more confident lenders will feel about financing it.

CLOSER LOOK Don’t forget the planning consentLenders won’t even look at your application unless it has planning permission – so get this in place before you submit. How much does it cost to get planning permission for a self build in the UK? As of the 6th December 2023, planning application fees for self builds in England rose by 25% across the board and are now as follows: Full Planning Application FeesFull planning applications require you to submit an application containing all the details relating to a particular development. This is necessary if you’re building a new house or if you’re significantly altering a domestic property.

Outline ApplicationsAn outline planning application is made when you’re looking to find out whether your proposed developments/plans are going to be acceptable either in principle, in whole or just in part. Generally, an outline planning application requires less information.

|

Since self build mortgages rely on stage releases, the lender wants to know that each drawdown of funds will be enough to keep the project progressing. They’ll also want reassurance that you’re not going to run out of money part way through the build. It is therefore essential that you put together a detailed budget that proves you understand the various costs involved in your project, leaving nothing to guesswork.

After years of searching for their forever home, Arthur and Lydia Achard turned to a rural plot in Northumberland. The couple teamed up with Giles Arthur Architects to design the home, with Fleming Homes delivering the timber frame, insulation, windows, doors and joinery. The 518m² self build cost £500,000 (£965 per m²). Photo: Kate Buckingham

Using the Build It Estimating Service is a good first step, as this will enable you to better understand the figures that trades put forward. But your budget should also be backed up with multiple quotes to show your figures are realistic and reliable.

Things don’t always go to plan, so the lender will expect to see a contingency of around 10-15% of the construction costs. The contingency must reflect the risks, so to keep this minimal, deal with any problem areas and cut out complexity at the design stage.

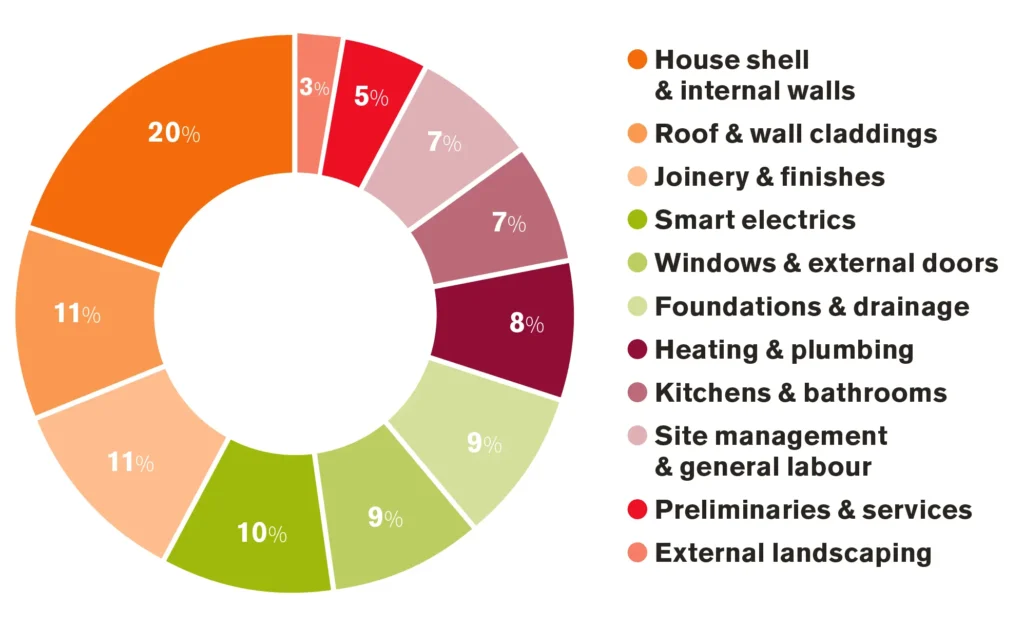

FAQ How much does it cost to build a house?A middle-of-the-road figure for how much it’ll cost to build a house in the UK would be around £2,200+ per m². This is on the assumption you’ll be doing some of the project management and mostly using experienced trades to finish your scheme. At this kind of price point, you can expect an average self build spec – but still better quality than a typical developer house. The price per m² will rise significantly if you want to increase the quality or intend to hand the project over to the professionals (expect to pay at least £2,750 per m² for a main contractor build, for instance). On the basis of £2,200 per m², if you wanted to self build a 200m² home, it would cost you around £440,000 for the construction and fit-out costs. How you apportion your construction and fit-out budget will come down to your individual project goals, priorities and build route (for instance, you might apportion a bit more to a prefabricated house shell that saves you money elsewhere; opt for standard electrics rather than a smart home; or self-manage to cut out some site management costs). Nevertheless, this pie chart will give you a useful starting point to gauge where your money is likely to go.

|

Self build mortgages aren’t as straightforward as traditional mortgages, so clear communication is essential. You’ll need to provide proof of income, your credit history, your build’s budget, and any other financial info they request. Present the information as clearly as possible so it can be fully considered by the lender. They will value honesty and prefer borrowers who are upfront about any risks or challenges, so don’t hide potential issues.

Getting a self build mortgage may be more work than a standard loan, but with a strong credit score, clear plans, careful budgeting and a little financial tidying, you can position yourself as a strong applicant and secure the funds you need. Remember, the more prepared you are, the easier it will be to show lenders that you’re ready to take on a self build and that you’re financially equipped to see it through to completion.

| Want to chat to the right people about finance and self build mortgages?

Build It Live is the place to do it! Why not visit the Build Cost Clinic and learn more about how much your project will cost? Build It Live takes place three times a year in Exeter, Kent and Malvern. The next show will be on 12th and 13th September 2026 in Exeter, Devon. Claim a pair of free tickets today and start planning your visit. |

Featured image: iStock Natee Meepian

Login/register to save Article for later

Login/register to save Article for later